ACCR2026-04-23T00:00:00Zhttps://www.accr.org.auACCRoffice@accr.org.au“Show of force”: Investors deal blow to BP on oil and gas spending 2026-04-23T00:00:00Zhttps://www.accr.org.au/news/“show-of-force”-investors-deal-blow-to-bp-on-oil-and-gas-spending/ACCR is commenting on the results of today's BP AGM, in particular:

25.85% of BP shareholders voted in support of shareholder-proposed resolution 24, requesting disclosures on capital discipline on oil and gas investments, filed by Nest, Greater Manchester Pension Fund, Merseyside Pension Fund, London CIV, Wales Pension Partnership, and PUBLICA, together with ACCR.

This is the highest ever vote of support for a management-opposed resolution at BP.

52.53% of shareholders voted against management-proposed resolution 23 to revoke previous climate-related reporting, which failed to reach the required 75% threshold to pass

52.88% voted against management-proposed resolution 22 to permit virtual-only AGMs, which failed to reach the required 75% threshold to pass

18.23% voted against resolution 4, the election of the Chair, Albert Manifold

Commenting on the results, Nick Mazan, Oil and Gas Strategy Lead, ACCR, said:

“Today’s result is unprecedented and demonstrates that investors are fed up with BP’s lack of capital discipline and its approach to shareholder rights.

“This collective show of force puts the new BP leadership team on notice: the company must show its planned surge in upstream investment can deliver shareholder value.

“Investors have seen the numbers – and the numbers don’t lie. It’s encouraging to see over a quarter of shareholders challenging management on upstream spending given the low returns on investment to date, coupled with the uncertain demand outlook for high-cost oil and gas as the world electrifies at speed. BP and other oil and gas companies would do well to take note of today's result and to reconsider their default to volume growth.

“In our view it was a mistake for BP to expect to push through measures to undercut shareholder rights without resistance. Investors have communicated loud and clear to the company that brushing shareholders aside is unacceptable in public markets.”

Diandra Soobiah, Director of Responsible Investment at Nest, said:

“This level of support signals that investors want firmer assurances on BP’s oil and gas capital discipline—and clearer evidence of how it safeguards long-term shareholder value.

We want BP to reflect on how it can reassure investors, through clear, practical and comparable disclosures, that increased oil and gas expenditure will improve performance and deliver value for shareholders.”

Cllr Doug McMurdo, Chair of LAPFF, said:

“We look forward to BP’s plan to satisfy investors who voted in droves for quality information on how its new oil and gas investments will deliver long-term value for shareholders. We are disappointed at the recent behaviours of the company - namely, weakening governance, reducing transparency, and rolling back climate commitments - and hoped that a change in leadership would have put a stop to the “BP reset” mantra pushed throughout 2025.”

Background

Under the UK Corporate Governance Code, where there has been a vote of 20% or above against management, the company should set how it will consult shareholders to understand the reasons behind the result. It should also report back on its consultations 6 months after the AGM, and again in the annual report, where it should explain the impact that shareholder feedback has had on board decisions or proposed actions.

]]>Major proxy advisor and investor back shareholder resolution at BP2026-04-08T00:00:00Zhttps://www.accr.org.au/news/major-proxy-advisor-and-investor-back-shareholder-resolution-at-bp/ACCR is commenting on Reuters reporting that proxy advisor Glass Lewis, one of the two large proxy advisors, has recommended shareholders vote for ACCR’s resolution at BP, co-filed with institutional investors in advance of BP’s AGM, which will be held on 23 April 2026.

At the same time, Legal & General Investment Management, a top-ten shareholder in BP, has announced its intention to vote for the same resolution, along with its intention to vote against management in relation to number of other resolutions on the company’s AGM ballot.

Commenting on this, Nick Mazan, Oil and Gas Strategy Lead, ACCR, said:

“Glass Lewis' recommendation to vote for our co-filed investor resolution, which L&G is now backing, will likely send alarm signals across the BP boardroom. There is now clear and growing evidence that investors want to see BP apply a disciplined approach to its upstream business and justify how its new oil and gas spending will deliver returns for shareholders.

"Given that the two major proxy advisors have now recommended a vote against management across multiple items on the ballot, BP’s board has serious questions to answer about how it manages shareholder dissent. A more productive approach to governance and shareholder engagement is required as we approach a monumental AGM for the oil and gas major.”

Background:

Glass Lewis recommended voting against management on resolution 23 (to revoke previous climate reporting requirements introduced by majority-supported shareholder resolutions), resolution 24 (the institutional investor-filed resolution coordinated by ACCR), and resolution 4 (the election of Chair Albert Manifold.)

L&G has made public its intention to vote against management on resolutions 22,23, 24 and 4.

ISS, the other major proxy advisor, recommended voting against management on resolutions 22 (to move to virtual-only AGMs) and 23.

]]>Shareholder rights in Japan must be upheld – ACCR comment2026-03-19T00:00:00Zhttps://www.accr.org.au/news/shareholder-rights-in-japan-must-be-upheld-–-accr-comment/ACCR is responding to comments made by Nippon Steel’s CEO advocating for the abolition of certain shareholder rights in the Companies Act, as an interim draft proposal for changes to the legislation was published yesterday.

The Japanese Ministry of Justice’s Legislative Council met on 18 March to agree options for changes to the Companies Act that would make it harder for shareholders to file proposals at company AGMs. Options reportedly include abolishing the “300 voting rights” threshold, a key right of shareholders.

Last week at the Council for Japan’s Growth Strategy meeting, hosted at the Prime Minister's Office, Nippon Steel’s CEO Mr Eiji Hashimoto also advocated to remove this right. He called it “unreasonable, forcing unnecessary responses to proposals that are almost never passed,” saying “it should be abolished promptly.”

ACCR is concerned that scrapping the 300 voting rights threshold will significantly constrain the ability of even large institutional investors to file proposals. Very few investors have holdings in Nippon Steel over 1% and foreign investors filing proposals via the 1% threshold, individually or as a group, must make complex submissions under the Foreign Exchange and Foreign Trade Act prior to making a proposal.

Commenting on the statements by Nippon Steel, Martin Norman, Head of Stewardship, Global, ACCR, said:

“Large institutional investors have a mandate to invest over the long term. It is counterproductive to restrict their rights to file proposals on issues that are highly relevant to shareholders. This also goes against the spirit of Japan’s Corporate Governance Code, which prioritises ‘securing the rights and equal treatment of shareholders, and dialogue with shareholders.’

“Rules for filing shareholder proposals in Japan should align with international best practice, as was intended when they were designed. Other jurisdictions have developed effective checks and balances to ensure that shareholder proposals are appropriate while protecting shareholders’ rights.

“ACCR has filed and co-filed shareholder proposals in Japan, including with Nippon Steel, facilitating sincere and productive dialogue between companies and shareholders, for the benefit of all parties involved.

“Given ACCR’s recent history of engagement with Nippon Steel, we are concerned to see these comments from the company’s CEO, which create unnecessary friction between shareholders and Nippon Steel when investors in Japanese equities are seeking certainty during significant domestic and global upheaval. We believe Nippon Steel could use its privileged position, as one of only eight committee members at the Cabinet-level meeting, to advocate for matters which more clearly contribute to Japan’s growth strategy.”

Background

On the changes to the Companies Act

The Japanese Ministry of Justice’s Legislative Council is currently considering multiple proposed changes to the Companies Act which may negatively impact shareholder rights in Japan. A meeting to approve an interim draft of proposed changes to the Companies Act was held on 18 March. The interim draft is likely to be available for public comment from late March to early May. For further information on proposed changes to shareholder rights in Japan, please refer to Client Earth’s briefing.

On the “300 voting rights” threshold

300 voting rights equate to 30,000 shares at JPX-listed companies, including Nippon Steel. One unit of 100 shares equals one voting right. Under the Companies Act, shareholders may currently file a proposal if they continuously hold at least 1% of the total voting rights or at least 300 voting rights in the preceding six months.

On Nippon Steel’s recent advocacy regarding changes to shareholder rights in Japan

Nippon Steel also advocated in July 2025 for the same voting rights to be abolished, and for changes which could permit companies to limit discussion of shareholder proposals at AGMs based on the results of prior electronic voting or for procedural reasons.

]]>Liz Westcott becomes new CEO at Woodside2026-03-18T00:00:00Zhttps://www.accr.org.au/news/liz-westcott-becomes-new-ceo-at-woodside/The Australasian Centre for Corporate Responsibility (ACCR) is commenting on the appointment of Liz Westcott as the CEO of Woodside Energy Group.

Alex Hillman, Lead Analyst at ACCR said:

“Liz Westcott as CEO has an opportunity to stamp her own mark on Woodside and shape a company that adds value to shareholders as opposed to eroding value.

“Our analysis has shown that Woodside’s aggressive growth strategy has not translated into improved shareholder value. Like much of the oil and gas sector, Woodside demonstrates that more barrels do not automatically mean more value.

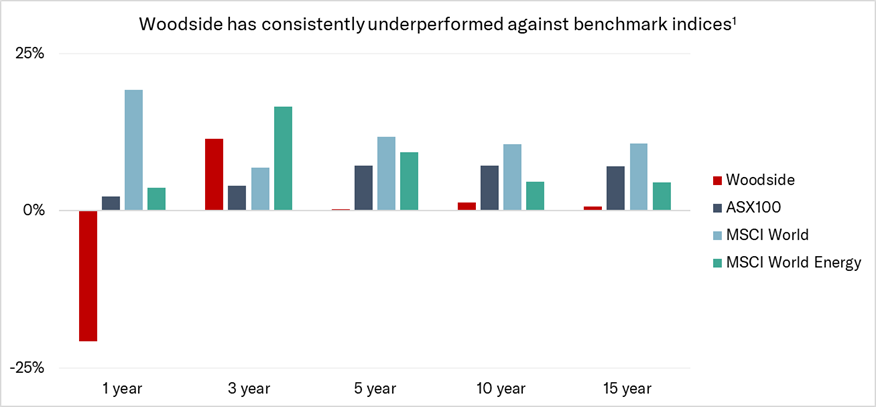

“Over the past five years, Woodside has doubled down on growth. Since 2020, the company has invested in around five billion barrels of new oil and gas supply, a strategy that is expected to lift production by roughly 370 per cent through the 2030s. Yet despite this, Woodside has consistently underperformed the sector, the Australian market and global equity markets, including over one-, three- and five-year periods.

“This includes during periods of global oil spikes such as with Ukraine.

“The evidence is clear: exploring for and developing conventional upstream projects has eroded shareholder value at Woodside.[1] Continuing with this strategy is unlikely to deliver the shareholder returns that investors prioritise.

“Investors will be hoping that Westcott can be a circuit breaker on Woodside’s habit of pursuing high-capex, marginal fossil fuel projects. While an internal successor, she has an opportunity to start focusing on better capital returns.

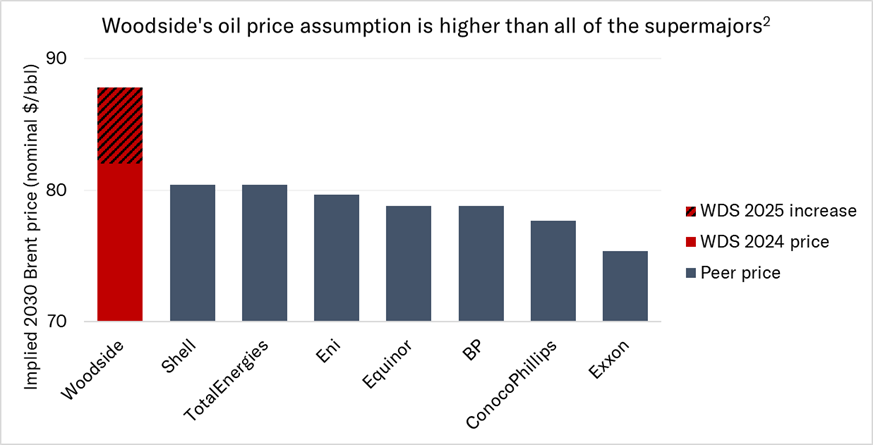

“Woodside has an opportunity to move beyond rhetoric with capital discipline and genuinely prioritise its shareholders. The board and the new CEO can now rethink the value destructive Browse project, which is more expensive than 70% of competing potential new gas supplies around the world, as well as the expansion of Louisiana LNG.”

Total shareholder return of Woodside has consistently underperformed the local market, global market and global sector

ACCR, 2025, When growth no longer pays. In addition to this research, which addressed the value oil and gas companies can deliver by moving away from conventional exploration and upstream development, ACCR published research that addressed the need for greater capital discipline at BP (Moving BP from rhetoric to action on capital discipline) in late 2025. ↩︎

]]>ACCR to appeal Federal Court judgment2026-03-18T00:00:00Zhttps://www.accr.org.au/news/accr-to-appeal-federal-court-judgment/The Australasian Centre for Corporate Responsibility (ACCR) has appealed the decision of Justice Markovic in the case of ACCR v Santos Ltd.

In 2021, ACCR commenced landmark proceedings in the Federal Court alleging that Santos Ltd breached provisions of the Corporations Act 2001 (Cth) and the Australian Consumer Law by engaging in misleading or deceptive conduct relating to representations in its 2020 Annual Report, 2020 Investor Day Briefing and 2021 Climate Change Report.

Last month the Federal Court dismissed those claims.

Commenting on ACCR’s decision to appeal, Brynn O’Brien, Co-CEO of ACCR said:

“This case concerns fundamental legal standards that apply to all businesses in Australia responding to climate change, and which are central to the integrity of market disclosures. The legal issues raised in the judgment warrant clarification by an appellate court.

“In our view, the judgment sets the bar for corporate communication about climate commitments well below market and investor expectations. We think it increases the burden on investors to interrogate the full context in which claims are made, and the assumptions, uncertainties, and emerging technologies that may underpin them.

“Businesses doing hard, evidence-driven work in the energy transition need clear guidance on the standards governing climate disclosures.

“ACCR has engaged the specialist corporate and consumer law team at Webb Henderson on appeal, and will continue to be represented by our counsel team Noel Hutley SC, Sebastian Hartford-Davis, Jerome Entwisle and Zoe Bush. We thank the Environmental Defenders Office (EDO) for their professionalism, dedication and effort in the case at first instance.”

Background

Court file access: To request a copy of the Notice of Appeal please contact the NSW Registry of the Federal Court by email at nswreg@fedcourt.gov.au or by phone on 1300 720 980, providing the proceeding reference (Matter No NSD414/2026 ACCR v Santos Ltd) and follow the Registry’s instructions.

]]>Shell’s LNG strategy update – fundamental flaws remain2026-03-17T00:00:00Zhttps://www.accr.org.au/news/shell’s-lng-strategy-update-–-fundamental-flaws-remain/ACCR is commenting on Shell’s LNG Portfolio – Strategic Spotlight, which comes as a result of over a fifth of shareholders supporting a shareholder resolution co-filed by ACCR and institutional investors last year.

The resolution asked Shell to justify the assumptions behind its LNG growth strategy and explain how it’s consistent with the company’s climate commitments.

It was filed by Brunel Pension Partnership, Greater Manchester Pension Fund and Merseyside Pension Fund, which have combined assets under management of US$86 billion.

Nick Mazan, Oil & Gas Strategy Lead, ACCR, said:

“While Shell has produced a more sophisticated document than its previous LNG Outlooks and also made some important concessions, including that LNG utilisation may fall during periods of low price, it continues with fundamental flaws that we’ve seen in Shell’s previous LNG disclosures.

“It does not explain how LNG will outcompete other sources of energy – like renewables – which are cheaper and faster growing. For example, outcompeting renewables for electricity would require gas to be priced below $5/MBtu, but all of Shell's new projects cost more than that.

“Industrial demand remains a central component to Shell’s view of natural gas demand growth. Despite this being an area of engagement for investors, it's disappointing not to see a stronger focus on this apparent driver of demand, and instead a focus on more marginal demand drivers such as buildings and transport.

“In terms of financial resilience, Shell invests in infrastructure that will produce LNG for decades. Yet it is only disclosing LNG contracting information to 2029. Its most aggressive low-cost sensitivity still only applies low costs from 2036 - leaving a gap from 2030 to 2035 where Shell says little about the resilience of its portfolio.

“Shell fails to see that LNG is a risk to energy security. There have been two major geopolitical crises this decade that have caused LNG price spikes and exposed LNG as an unreliable energy source in consumers’ eyes. Shell has not explained how LNG’s reputation as an expensive fuel can be rehabilitated.

“Shell continues to see LNG as its largest contribution to the energy transition, however, given the relative emissions of LNG, it remains unclear how this is compatible with its 2050 net zero ambition.”

]]>ACCR comment on Federal Court ruling2026-02-23T00:00:00Zhttps://www.accr.org.au/news/accr-comment-on-federal-court-ruling/Today Justice Markovic published her reasons for judgment in the case of ACCR v Santos Ltd.

The case contended that Santos Ltd had engaged in misleading or deceptive conduct in its 2020 Annual Report, 2020 Investor Day Briefing and 2021 Climate Change Report.

Commenting on the Court’s reasons for dismissing the case, Brynn O’Brien, Co-CEO of ACCR said:

“This case was always about market integrity and ensuring rigour in disclosures.

“Santos is immensely capable of long-term planning and analysis, and investors expect that expertise to be applied to climate risk and mitigation.

“This was the first court case in the world to test a company’s net zero claims, and it has helped drive significant improvements in climate reporting in the Australian market and internationally. It is disappointing that, in our view, the Court’s decision has not reinforced these advancements.

“Santos argued, and the Judge accepted, that it was not misleading in the circumstances for Santos to say:

‘clean fuel’ in relation to gas to convey that gas is ‘cleaner than coal and diesel’ on consumption;

‘zero emissions hydrogen’ to convey ‘hydrogen produced from natural gas with CCS and offsets’;

it had ‘a realistic roadmap, real activities and a plan to achieve net zero by 2040’ in the context of announcing a ‘long-term target that predicts what Santos can do if markets, technologies and regulatory regimes emerge as anticipated’.

“While we respect the judgment of the Court on this matter, and accept the findings that Santos did not engage in wrongdoing, our view is that the nature of this clarification of Australian consumer and corporations law puts an enormous burden on investors to interrogate the true meaning of corporate disclosures, including ambiguous language and assumptions.

“This was an important case. Whether the ruling ultimately helps or hinders companies trying to convince investors of their climate strategies remains to be seen. We will take time to review it carefully before considering next steps and our options.”

Background

In 2021, the Australasian Centre for Corporate Responsibility (ACCR) represented by the Environmental Defenders Office along with Noel Hutley SC, Sebastian Hartford-Davis, Jerome Entwisle and Zoe Bush, commenced landmark proceedings in the Federal Court alleging that Santos Ltd breached provisions of the Corporations Act 2001 (Cth) and the Australian Consumer Law by engaging in misleading or deceptive conduct relating to representations in its 2020 Annual Report, 2020 Investor Day Briefing and 2021 Climate Change Report.

This was the first court case in the world to challenge the veracity of a company’s ‘clean energy’ claims and its pathway to net zero.

The key allegations of misleading and deceptive conduct concerned three major areas:

representations that Santos is a producer of “clean energy” and that natural gas is a “clean fuel”.

representations that hydrogen produced by Santos from natural gas with carbon capture and storage (blue hydrogen) is “clean hydrogen” and “zero emissions hydrogen”.

representations that Santos had a clear and credible pathway to ‘net zero’ by 2040.

The Court heard the matter over three weeks in October, November and December 2024.

]]>MEDIA ALERT: ACCR v Santos Ltd - Judgment2026-02-16T00:00:00Zhttps://www.accr.org.au/news/media-alert-accr-v-santos-ltd-judgment/What: Judgment, Australasian Centre for Corporate Responsibility v Santos Ltd

Where: Court Room 18C, Federal Court of Australia, 184 Phillip Street, Sydney NSW 2000.

When: 9.30am, Tuesday 17 February 2026.

Video streaming: If you wish to observe the delivery of judgment, we recommend making a request via email to the Federal Court nswreg@fedcourt.gov.au and include reference to the proceeding number (NSD858/2021).

Court file access: To request a copy of court documents contact the NSW Registry of the Federal Court by email at nswreg@fedcourt.gov.au or by phone on 1300 720 980, providing the proceeding reference (Matter No NSD858/2021 ACCR v Santos Ltd) and follow the Registry’s instructions.

Background

In 2021, the Australasian Centre for Corporate Responsibility (ACCR) commenced landmark proceedings in the Federal Court of Australia alleging that Santos Ltd breached provisions of the Corporations Act 2001 (Cth) and the Australian Consumer Law by engaging in misleading or deceptive conduct relating to representations in its 2020 Annual Report, 2020 Investor Day Briefing and 2021 Climate Change Report.

This was the first court case in the world to challenge the veracity of a company’s ‘clean energy’ claims and its pathway to net zero.

The key allegations of misleading and deceptive conduct concern three major areas:

representations that Santos is a producer of “clean energy” and that natural gas is a “clean fuel”.

representations that hydrogen produced by Santos from natural gas with carbon capture and storage (blue hydrogen) is “clean hydrogen” and “zero emissions hydrogen”.

representations that Santos had a clear and credible pathway to ‘net zero’ by 2040.

The Court heard the matter over three weeks in October, November and December 2024.

Media contact:

Kate Sieper (AU) - M +61 466 745 615

]]>New research: billions of reasons to consider new Woodside strategies2026-02-12T00:00:00Zhttps://www.accr.org.au/news/new-research-billions-of-reasons-to-consider-new-woodside-strategies/The departure of Woodside’s CEO offers the company the perfect opportunity to explore alternative strategies that could deliver billions of dollars more value for shareholders, new ACCR research finds.

Fork in the road examines Woodside’s pursuit of an aggressive growth strategy across its FID projects since 2020, finding that while the company has increased production, it has not delivered value for shareholders. As Woodside searches for a new CEO following Meg O’Neill’s departure, the report recommends that shareholders engage with Woodside’s board on a refreshed capital allocation strategy that emphasises greater returns.

Key findings include:

At this point in time, ceasing oil and gas exploration and development would generate almost $3 billion more NPV than a business-as-usual strategy for Woodside.

Woodside’s four major oil and gas projects – Sangomar, Scarborough, Trion and Louisiana LNG – that reached FID since 2020 have eroded $3.5 billion of value (NPV), despite the projects collectively increasing scope 3 emissions by 2.5 GtCO2e (Woodside’s share of these emissions is 1.4 GtCO2e).

Woodside has consistently underperformed the ASX100, MSCI World and MSCI World Energy indices across a three-, five-, ten- and 15-year period.

Woodside has not made a material exploration discovery in 20 years, since Pluto (2005/06).

Woodside has significantly increased its exposure to LNG at a time when there are risks of oversupply and uncertain demand, which may affect the financial performance of the Scarborough and Louisiana LNG projects.

Commenting on the research, Alex Hillman, Lead Oil and Gas Analyst, ACCR, said:

“Under Meg O’Neill’s leadership, Woodside succeeded in increasing production, but it failed on delivering strong shareholder returns.

“Woodside’s recent projects have eroded value and its upcoming projects look even more underwhelming. Its LNG projects are high cost, its gas projects are uncompetitive and its largest oil project is immaterial. Despite spending half a billion dollars each year exploring for new oil and gas, Woodside hasn’t made a meaningful new discovery in 20 years.

“Woodside has shown that more oil and gas production does not equal more value. With the search for a new CEO underway, now is the time for investors to engage with Woodside’s board on a strategy that increases returns.

“Now is a good time for investors to ask Woodside to recalibrate its investment assumptions and dramatically pull back on its exploration program. Woodside should also stop rewarding executives for production growth that doesn’t also improve shareholder value.

“Investors can drive an honest conversation about Woodside’s sustained underperformance and help prevent Woodside investing in more unattractive projects.”

]]>BP cuts distributions – yet continues to favour oil & gas growth2026-02-11T00:00:00Zhttps://www.accr.org.au/news/bp-cuts-distributions-–-yet-continues-to-favour-oil-gas-growth/ACCR is commenting on BP’s 2025 full year results.

Nick Mazan, Oil & Gas Sector Strategy Lead, ACCR, said:

“By cutting its shareholder distributions while continuing to funnel capex into the upstream business, BP doesn’t appear to have shareholder interests at heart.

“Shareholders want to see returns from oil and gas companies, particularly when the longer-term outlook for oil and gas is so uncertain. Axing the share buyback programme could be sign that BP doesn’t have confidence in the market outlook or its operating assets.

“While the pivot back to oil and gas has been justified by scapegoating the low carbon business, our analysis shows that the upstream business has been the source of 75% of disposal losses and impairments since 2020.

“BP’s upstream capital allocation is a cause for concern. Over the past 5 years the company has invested $22bn in the upstream business, which will deliver less than $1bn under forward prices. For example, last year, BP made a final investment decision on Tiber, a $5 billion oil project, despite data from Rystad Energy showing that it’s more expensive than 81% of competing oil projects. Looking forward does not offer much promise for shareholders either, with BP’s pre-FID portfolio not having a competitive advantage.

“Long-term investors want to see BP taking a genuinely disciplined approach to capital allocation to protect shareholder value.”

]]>75% of BP’s disposal losses & impairments since 2020 down to oil and gas2026-02-09T00:00:00Zhttps://www.accr.org.au/news/75-of-bp’s-disposal-losses-impairments-since-2020-down-to-oil-and-gas/75% of BP's disposal losses and impairments have come from its oil and gas business over the past five years, a new analyst note by ACCR finds, challenging the common narrative that the company’s renewables investments are the main driver of its underperformance.

The note comes ahead of BP’s Q4 2025 earnings tomorrow, where the oil and gas major is expected to report impairments of $4-5 billion in its transition business. While these impairments are material, this represents less than 10% of BP’s disposal losses and impairments since 2020.

Most of the impairments since 2020 relate to either project cost overruns and delays, or the company’s exit from its Russian oil business, the research finds. Effective project execution is critical for projects to be delivered on budget.

Last week, institutional investors filed a shareholder resolution calling on the company to demonstrate how its surge in upstream spending, announced last year in its strategic reset, will deliver value for shareholders. Part of the resolution asks BP to disclose how it accounts for cost overruns and delays in project schedules, and how they are integrated into the investment framework, given the poor historical track record across the industry.

Today’s note is consistent with past ACCR research showing that value in the oil and gas sector has been materially eroded by its upstream investments. For example, BP’s $22 billion investment in new conventional oil and gas projects over the past six years has only created $0.9 billion in shareholder value under forward prices.

Nick Mazan, Oil & Gas Sector Strategy Lead, ACCR, said:

“BP seems to be pointing to a cracked window while the foundation of the house is quietly sinking. The attention given to the recent impairments in BP's transition business is misdirected, when the upstream business deserves just as much discredit. Increasing capex in an underperforming business like oil and gas makes little sense to investors who would benefit more from the company showing capital discipline across its whole business, not just renewables, especially at a time when the demand outlook for oil and gas is so uncertain, and supply is expected to outstrip demand over the coming few years.”

]]>Shareholder Resolution to BP plc on Upstream Capital Expenditure Disclosures2026-02-03T00:00:00Zhttps://www.accr.org.au/posts/shareholder-resolution-to-bp-plc-on-upstream-capital-expenditure-disclosures/This shareholder resolution is co-filed by UK and European pension funds, along with ACCR, including: Nest, London CIV, Wales Pension Partnership, Greater Manchester Pension Fund, Merseyside Pension Fund, and PUBLICA. More than 100 individual shareholders also supported the filing.

This page contains the resolution and supporting statement.

Special Resolution

Shareholders direct the Company to disclose how it promotes a disciplined approach to capital expenditure in order to generate an acceptable return on capital for each new material oil and/or gas project of the Company (‘Project’).

Such disclosures shall include an explanation of whether and how the Company:

assesses the relative cost competitiveness of each Project;

accounts for cost overruns and delays in project schedules; and

demonstrates how continued exploration capex creates value for shareholders.

These disclosures shall be made, to all Shareholders, by no later than the 2027 Annual General Meeting and shall include the principal criteria, data sources, methodologies and assumptions used to underpin these claims with reasonable detail, but without disclosing any specific matters which are commercially sensitive.

Supporting Statement to Special Resolution

This proposal seeks enhanced disclosure for BP shareholders, allowing them to better assess whether and how the company’s investment decision-making promotes disciplined capital allocation.

Shareholders have legitimate reason to question BP’s approach to capital allocation due to its long-term relative underperformance, even within a materially underperforming sector. The MSCI World Energy Index has delivered 116% lower returns than the MSCI World Index over the last ten years and lower returns than all bar one other MSCI sector. BP has further underperformed the MSCI World Energy Index over three, five, ten, 15 and 20 years.[1]

Against this backdrop, it is further cause for concern to shareholders that the Company now plans to grow its upstream investment. From 2022 to 2024, BP allocated $9 billion[2] p.a. of capex to its upstream business, which is about 60% of its total capex.[3] Following the strategic reset announced at the 2025 Capital Markets Day (CMD), this is due to increase to around $10.5 billion p.a., or 75% of all capex.[4]

A disciplined approach to capital expenditure is critical to ensuring that the Company limits its investment to projects that provide adequate returns to shareholders in the future. While the Company acknowledges the importance of capital discipline, it is unclear how this is being integrated into upstream investment decision-making. The disclosures sought by this shareholder proposal therefore aim to provide greater clarity.

There is no one way to ensure a disciplined approach to capital expenditure, rather it is important that the Company demonstrates to shareholders how, across a broad range of approaches, profitability is prioritised. Currently, the Company primarily relies on commodity price assumptions and hurdle rates to demonstrate its resilience. However, the prices currently applied in the investment framework are 16% above the forward market price.[5] As such, this proposal seeks to improve disclosure of the company’s approach to capital discipline with particular reference to three key elements of the investment framework.

Cost-competitiveness

A pre-FID project’s position on the cost curve is an important measure of its resilience and competitiveness in a global, liquid market. Projects higher on the cost curve are at higher risk of value erosion under a lower price environment. BP’s current disclosures do not indicate how the Company’s capex decisions account for a project’s relative cost-competitiveness. This is despite a shareholder proposal supported by BP and over 99% of its shareholders in 2019,[6] which stated in the supporting statement that the Company should consider the “potential return on investment and consideration of their competitive positioning” when making FID on new material oil and gas projects.[7]

ACCR research finds that BP’s gas assets are, on average, more expensive than 76% of global pre-FID supply, and its pre-FID oil assets are more expensive than 53% of global pre-FID supply.[8] This indicates a significant risk of value erosion for shareholders by BP sanctioning projects that are not competitively advantaged, suggesting a need for greater transparency from the company as to how it assesses project competitiveness when making FIDs. More recently, the sanctioning of the $5 billion Tiber project is a demonstration of the salience of this risk, with this project being more expensive than 81% of all unsanctioned oil projects, according to data from Rystad.[9]

Project execution

Research consistently shows that poor project execution is prevalent in the oil and gas sector, with studies indicating that projects range from an average of 17% to 59% over budget.[10] It is not clear from BP’s disclosures:

a) whether its track record of project execution is in line with its industry;

b) how project execution assumptions based on its track record are integrated into investment decision-making.

If BP’s investment framework does not use realistic assumptions about the prospects of its projects incurring cost and schedule overruns, this could cause it to systematically overvalue pre-FID projects. ACCR’s research shows that if BP is not integrating assumptions around project execution, such as cost overruns and project delays, then it could be overvaluing its conventional pre-FID assets by 40%.[11]

Exploration

Over the past three years, BP has spent an average $1.4 billion per year on conventional exploration,[12] and at its 2025 CMD it announced a plan to "reload the exploration hopper”.[13] Yet BP's rationale for continued exploration capex is unclear when viewed against the long-term, global trends in oil and gas exploration; and against its own exploration track record.

It is more important than ever that shareholders have good oversight of exploration expenditure. Since 2000, the average dollar that the oil and gas industry has spent on conventional exploration has eroded 71 cents (ACCR analysis of Rystad Energy data).[14] BP's conventional exploration has become less successful and more expensive over time, with ACCR research showing that the Company’s conventional exploration success rates have halved for licenses awarded since 2010, while its discovery costs have been growing.[15]

It is not clear from BP’s disclosures whether the Company’s investments in exploration perform any better than the sector, or whether its exploration capex creates or erodes value for shareholders.

Bloomberg Finance LP, Used with permission of Bloomberg Finance LP. ↩︎

]]>BP under pressure over undisciplined capital allocation - investors file shareholder resolution2026-02-03T00:00:00Zhttps://www.accr.org.au/news/bp-under-pressure-over-undisciplined-capital-allocation-investors-file-shareholder-resolution/Institutional investors, concerned about BP’s undisciplined capital allocation on oil and gas projects, have filed a shareholder resolution calling on the company to demonstrate how its surge in upstream spending will deliver value for shareholders.

BP is under pressure from investors due to its long-term underperformance. ACCR research shows that BP’s total shareholder returns (TSR) have underperformed both the market and its peers over three, five, ten and 15 years.[1] As part of a “reset” announced in 2025, BP is increasing spending on its upstream business by 17%. However, investors remain unconvinced this addresses the root cause of its underperformance and want to see evidence of greater capital discipline.

The shareholder resolution is co-filed by UK and European pension funds, along with ACCR, including: Nest, which serves a third of the UK workforce, London CIV, Wales Pension Partnership, Greater Manchester Pension Fund, Merseyside Pension Fund, and PUBLICA. Together the co-filing group manages £191 billion in assets.

The resolution asks BP to show how it takes a disciplined approach to capital expenditure, in order to generate an acceptable return on capital for each new oil and gas project. The requested disclosures are to include:

The relative cost-competitiveness of each project;

How the company accounts for cost overruns and delays in project schedules; and

A demonstration of how continued spending on exploration creates value for shareholders.

The investors filed the resolution following unsuccessful attempts to engage with the company.

Enhanced disclosures will give BP’s investors the insights they need to assess whether the company’s plans to increase upstream investments is a value-accretive strategy for them.

The resolution represents an opportunity for incoming CEO Meg O’Neill to demonstrate to shareholders that the company’s stated commitment to capital discipline is reflected in its investment decisions and strategy.

ACCR research shows that BP’s US$22 billion investment in new conventional oil and gas projects over the past six years has only created US$0.9 billion in shareholder value under forward prices.[2]

The resolution and supporting statement can be viewed here.

Nick Mazan, Company Strategy, UK Lead, ACCR, said:

“Investors need transparency to assess whether BP’s new spending will create value - or simply repeat past mistakes. Growing upstream exposure without demonstrating clear capital discipline is a red flag for shareholders.

“Our research shows that the $22 billion BP poured into conventional oil and gas projects over the past six years has delivered limited value to shareholders. This track record gives investors every reason to question why this strategy would deliver better results now, particularly as future demand conditions for oil and gas are highly uncertain.

“Investors would be concerned if the new CEO, Meg O’Neill, doesn’t take the opportunity to genuinely reflect on the numbers and poor returns from oil and gas growth projects and whether increasing upstream capex will create more shareholder value.

“The filing of this resolution demonstrates that investors are not willing to passively accept profligate oil and gas spending and are willing to use their stewardship rights assertively to hold BP to genuine capital discipline.”

Diandra Soobiah, Director of Responsible Investment at Nest, said:

“BP has underperformed for the past decade, including the period they were prioritising oil and gas production. Now they have dropped their renewables strategy, investors need to be reassured that any expansion to their upstream oil and gas portfolio will be governed by robust capital discipline and generate sustainable returns.

“Nest has engaged with BP since 2023. We view this resolution is an appropriate escalation of our engagement strategy, driven by our commitment to ensure the companies we invest in are appropriately managing transition risk

“Our ask is for BP to make practical disclosures on how they will deliver disciplined capital allocation and long-term performance. Clear evidence and comparable metrics will help Nest, and all shareholders, assess whether the company’s new oil and gas projects will truly create value into the future.”

Alison Lee, Responsible Investment Manager at London CIV, said:

“The appointment of a new Chair and CEO is an exciting development for BP shareholders. This leadership change brings an opportunity for fresh thinking and a clear, objective review of the best paths to long term value creation. As a shareholder, London CIV would especially like to see stronger disclosures to ensure investors can clearly identify whether BP’s plans to increase upstream investment represent a genuinely value accretive strategy.”

A spokesperson for Greater Manchester Pension Fund said:

“The world needs a managed decline in fossil fuels and spending more money on fresh oil or gas reserves without demonstrating clear capital discipline raises concerns for shareholders.”

Cllr Brenda Hall, Chair of Merseyside Pension Fund Pension Committee, said:

“The appointment of a new Chair and Chief Executive marks an important opportunity for BP shareholders. New ideas are clearly needed at the company, as is an objective investigation of the best pathways for creating shareholder value.”

Cllr Doug McMurdo, Chair, LAPFF, said:

“LAPFF would be seriously concerned if the new CEO, Meg O’Neill, doesn’t reflect on the poor returns from oil and gas growth projects and whether increasing upstream capex will create more shareholder value”

About Greater Manchester Pension Fund

Greater Manchester Pension Fund is the largest LGPS fund in the UK, managing over 30 billion pounds on behalf of approximately 400,000 members.

About London CIV

London LGPS CIV Ltd (‘London CIV’) is the investment pooling vehicle for London-based Local Government Pension Schemes (LGPS).

About PUBLICA

PUBLICA, the pension fund of the Swiss federal government and closely associated organisations, manages over 41 billion pounds on behalf of its 110’000 active members and pension recipients.

About Merseyside Pension Fund

Merseyside Pension Fund manages over 10 billion pounds on behalf of 153,000 active, deferred and pensioner members of the Local Government Pension Scheme (LGPS).

About Nest

Nest is the largest workplace pension scheme in the country, with more than 13 million members. That's one in three UK workers. By 2030, we expect that number to grow to half of the entire UK workforce. Nest invests £60 billion in assets on its members’ behalf.

About Wales Pension Partnership

The WPP is a collaboration of the eight Local Government Pension Scheme (LGPS) funds that cover the whole of Wales. Collectively, the WPP partner funds hold over £25 billion in assets under management, invested across a range of listed and private funds.

]]>Relining approval raises questions over Nippon Steel’s American plans2026-01-19T00:00:00Zhttps://www.accr.org.au/news/relining-approval-raises-questions-over-nippon-steel’s-american-plans/ACCR is commenting on U.S. Steel’s decision to approve the US$350 million relining of Blast Furnace No. 14 at Gary Works in Indiana, the United States of America.

The decision follows Nippon Steel Corporation’s acquisition of U.S. Steel in 2025 and locks in approximately 90 MtCO2 of emissions if the blast furnace operates for a full 20-year campaign life.[1] In 2024, Nippon Steel committed approximately $US300 million to relining the No. 14 Blast Furnace ahead of acquiring U.S. Steel.[2]

Commenting on the decision, Martin Norman, Investor Engagement Lead, ACCR said:

“With coal-free steelmaking an increasingly important factor in the American steel market, the decision to reline Blast Furnace No. 14 at Gary Works raises concerns for investors, who do not have clarity over U.S. Steel and Nippon Steel’s plans for managing the U.S. Steel blast furnaces imminently due for relining.

“Technology improvements from Japan that will increase efficiency are welcome, but decarbonisation targets from Japan also need to be brought to U.S. Steel. Decarbonisation targets for overseas assets should match domestic targets, with comprehensive transition plans outlining U.S Steel’s path to decarbonisation success.

“While Nippon Steel has expanded its decarbonisation ambitions by investing domestically in commercially ready solutions with significant emissions reduction potential, investors should engage constructively and critically with the company to ensure it applies a similar or greater level of ambition to the U.S. Steel assets.

“It is crucial that U.S. Steel secures its current and future competitiveness in an American steel market where low-carbon steel is already financially significant. Nippon Steel’s management of the U.S. Steel blast furnaces is a critical gauge of its ability to manage its whole portfolio’s emissions that investors need to watch closely.”

Global Energy Monitor, U.S. Steel ESG disclosures. Assuming a 90% blast furnace utilisation rate. ↩︎

]]>Meg O’Neill becomes new CEO at BP2025-12-18T00:00:00Zhttps://www.accr.org.au/news/meg-o’neill-becomes-new-ceo-at-bp/The Australasian Centre for Corporate Responsibility (ACCR) is commenting on the appointment of Meg O’Neill, the CEO of Woodside Energy Group, as BP's new CEO.

Brynn O’Brien, Executive Director of ACCR said:

“While BP has chronically underperformed the sector, Woodside has chronically underperformed BP.

“BP is right to be resetting its strategy and focusing on capital discipline to improve investor returns. However, Meg O’Neill is a curious choice in this context. Under O’Neill’s leadership Woodside has chased high-cost, marginal fossil fuel projects and not delivered satisfactory shareholder returns.

“The evidence is clear: exploring for and developing conventional upstream projects has eroded shareholder value at both BP and Woodside.[1] Continuing with this strategy will not deliver the shareholder returns that BP’s board says it is prioritising.

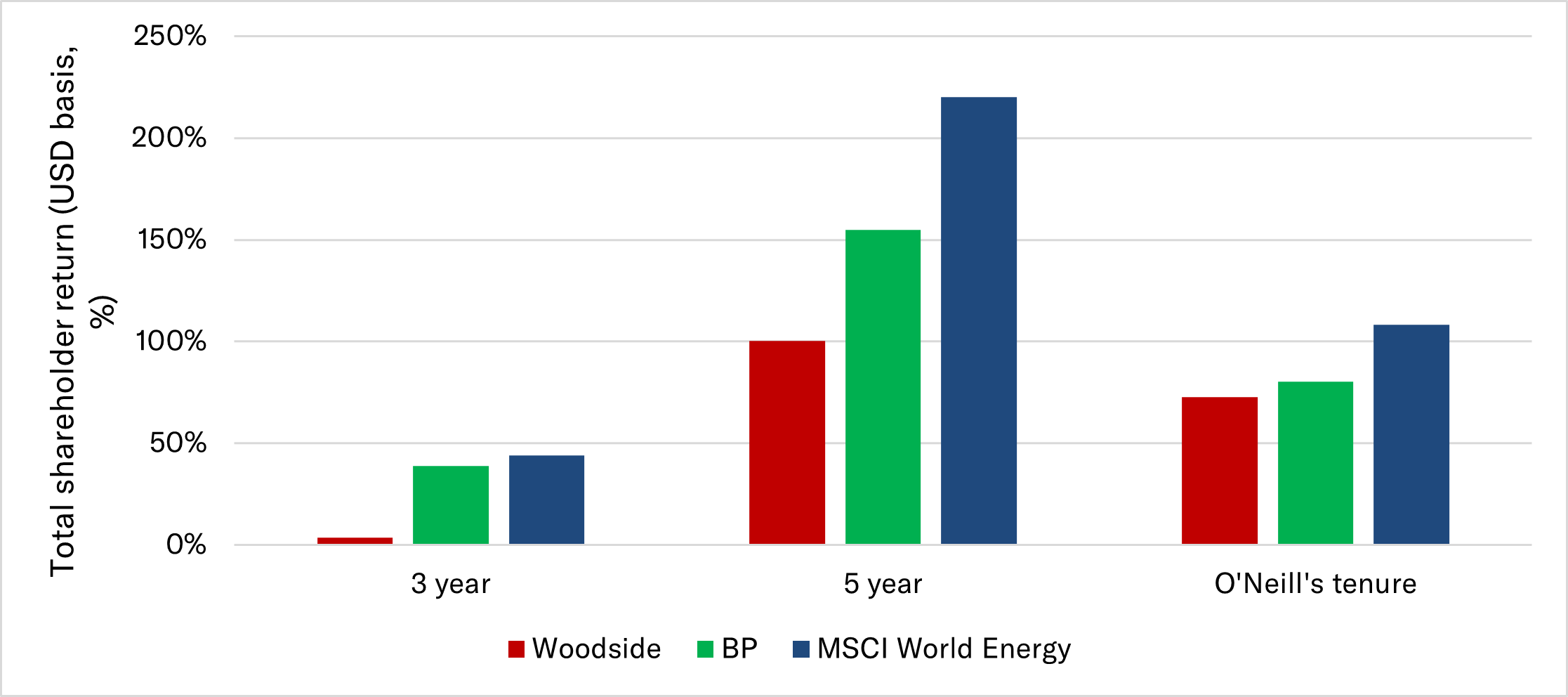

“At Woodside, O’Neill has overseen high-cost, high-emissions investments at a company that has delivered 1% p.a. total shareholder return (TSR) over 15 years and consistently underperformed its peers:

sanctioned a high-cost oil project in the Gulf of Mexico. Its partner Pemex has faced a string of safety and financial challenges [2]

acquired a high-cost, near-bankrupt LNG facility in Louisiana for over $1 billion.

“Woodside has been persistently unresponsive to shareholder concerns and under Ms O’Neill’s watch, has been the only company to suffer a majority vote against its climate plan. [3]

“At Woodside, O’Neill’s departure is an opportunity for a much-needed strategy refresh.

“Investors will be hoping that O’Neill’s departure is a circuit breaker on Woodside’s habit of pursuing high-capex, marginal fossil fuel projects, and is an opportunity to instead start focusing on better capital returns.

“Woodside has an opportunity to move beyond rhetoric with capital discipline and genuinely prioritise its shareholders. The board and the new CEO can now rethink the value destructive Browse project, which is more expensive than 70% of competing potential new gas supplies around the world, as well as the expansion of Louisiana LNG.”

Total Shareholder Return of BP, Woodside and the MSCI World Energy Index [4]

Background

[1]: ACCR, 2025, When growth no longer pays. In addition to this research, which addressed the value oil and gas companies can deliver by moving away from conventional exploration and upstream development, ACCR published research that addressed the need for greater capital discipline at BP (Moving BP from rhetoric to action on capital discipline) in late 2025.

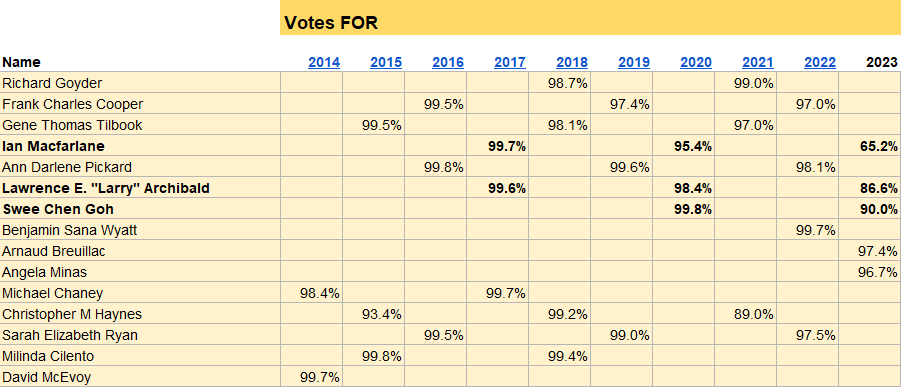

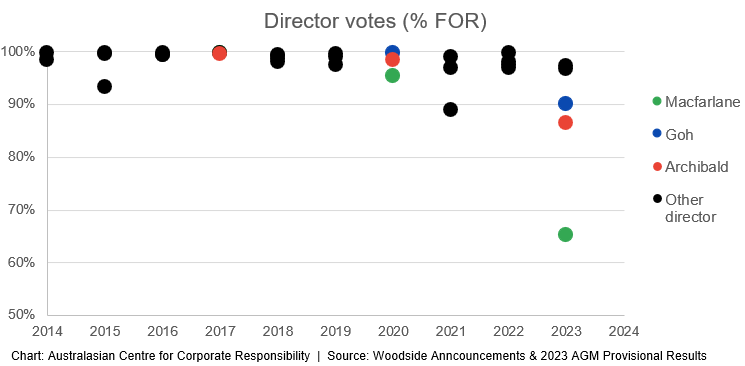

[3]: In 2024, Woodside shareholders delivered the worst Say on Climate vote recorded against a company climate plan (58.4%), beating the previous record set by Woodside in 2022 (48.97%). In addition to a worsening Say on Climate vote, the company has also faced persistently poor votes from shareholders against the re-election of its Directors:

2023 – Ian Macfarlane receives the worst vote recorded against a Woodside Director (34.81%)

2024 – Chairman Richard Goyder receives the worst vote recorded against a Woodside Chair (16.61%)

2025 – Sustainability Chair Ann Pickard receives the worst vote recorded against a sitting Woodside Committee Chair (19.45%).

[4]: Total shareholder return for 3 and 5 years are the periods ending 30 September 2025. “O’Neill’s tenure” is from 16 August 2021 to 30 November 2025

]]>New analysis: Oil and gas majors would create $78bn more value by stopping exploration2025-12-10T00:00:00Zhttps://www.accr.org.au/news/new-analysis-oil-and-gas-majors-would-create-78bn-more-value-by-stopping-exploration/Ten of the world’s largest oil and gas companies would create significantly more shareholder value by ending exploration and sharply curtailing upstream development, according to new analysis released today by ACCR.

“When growth no longer pays” assesses all the conventional oil and gas exploration and new projects the companies could invest in before 2035. It finds:

ceasing exploration and development of new projects and returning cash to shareholders would create a collective US$78 billion uplift in net present value (NPV)

across all ten companies, avoided exploration costs are the largest source of value

all ten companies would be more valuable as a production company, than as an exploration and production company.

The financial case for exploration is weak and getting worse. On average, every $1 spent on global conventional exploration by the sector since 2000 has eroded $0.71c. Conventional exploration is five times more expensive and taking almost twice as long compared to three decades ago.

If all ten companies ceased developing new conventional projects, they would remain large oil and gas producers for decades, with cumulative production reducing by 10% to 2050, compared to continuing a business-as-usual strategy.

Commenting on the research, Alex Hillman, Lead Analyst of the Australasian Centre for Corporate Responsibility (ACCR) said:

“The clearest path to shareholder value for oil and gas companies today is not chasing new barrels – it’s getting out of the value erosive exploration business and curtailing new conventional projects.

“Exploration isn’t creating value - it’s destroying it and has been for 25 years.

“Every one of the ten oil and gas companies we assessed is more valuable as a production company, rather than an exploration and production company.

“If creating shareholder value is the aim then ceasing exploration should be considered.

“Even if these companies ceased developing new conventional projects they would remain large oil and gas producers for decades. Cumulative production would reduce by 10% to 2050. And $78 billion of shareholder value would be created.

“Many investors would prefer to see a company give cash back to shareholders, rather than reinvest it in value erosive projects, even if it meant production gradually decreased.

Commenting on the research, Nick Mazan, ACCR Oil and Gas Strategy Lead, said:

“The oil and gas sector is running out of road. Exploration is slower, costlier, and eroding value, while the market itself is shrinking as more sectors electrify.

“This industry has delivered half the returns of the rest of the market over the last 10 years and continuing to plough shareholder money into upstream exploration and new projects will not change that.

“Oil and gas companies continue to underestimate the speed of technological change. The current oversupply in the market can largely be attributed to this, with little hope of improving circumstances in the future.”

]]>New research: New oil and gas investment will worsen BP’s performance woes 2025-11-26T00:00:00Zhttps://www.accr.org.au/news/new-research-new-oil-and-gas-investment-will-worsen-bp’s-performance-woes/BP’s US$22 billion investment in new conventional oil and gas projects over the past six years has only created US$0.9 billion in shareholder value under forward prices, according to new research from ACCR.

“Moving BP from rhetoric to action on capital discipline” finds BP could be US$11 billion more valuable if it stopped exploration and development relating to conventional oil and gas projects and focused on production only.

BP’s total shareholder returns (TSR) have underperformed both the market and its peers over three, five, ten and 15 years. At its 2025 Capital Markets Day, BP announced a “fundamental reset” of its strategy, pledging to grow long-term shareholder value. The company is reducing capex for its low-carbon energy business to less than $800 million per year, while simultaneously increasing upstream capex from $8.5 to $10 billion p.a and increasing exploration.

The research finds that BP’s conventional oil and gas portfolio awaiting Final Investment Decision (FID) is not cost competitive when compared to global supply. A change to BP’s upstream strategy – in particular, tightening its investment framework and ceasing conventional exploration – offers a more credible path to the value that shareholders expect.

Key Findings:

BP's $22 billion of conventional greenfield capex sanctioned over the last six years has created limited value for shareholders. The estimated net present value (NPV) of these projects is $0.9 billion under forward prices.

BP’s conventional pre-FID portfolio is not low on the cost curve. The company’s gas assets are, on average, more expensive than 76% of global pre-FID supply; and its oil assets are, on average, more expensive than 53% of global pre-FID supply.

We modelled the impact of BP stopping exploration and the sanctioning of conventional projects, finding the company would be $11 billion more valuable and still be a major producer, with 400 million boe in 2050. This suggests BP is more valuable as a production company than as an exploration and production company.

Globally, conventional exploration has been eroding value since the 1990s. BP's conventional exploration has become less successful, more expensive and less productive.

BP’s investment framework risks misallocating capital into low value projects. Under BP’s price deck, and assuming no delays or cost overruns beyond Rystad’s estimates, the value of BP's conventional pre-FID portfolio is $6-8 billion. Under forward prices, and adjusting for typical cost and schedule slips, this same portfolio would be worth 80-85% less.

Commenting on the research, Nick Mazan, ACCR Oil and Gas Strategy Lead, said:

“BP has significantly underperformed the sector and market more broadly over the past three, five, 10 and 15 years. Increasing exploration and doubling down on upstream capex is not a turnaround plan, it’s a rerun.

“The $22 billion BP has poured into conventional oil and gas projects over the past six years has delivered limited value to shareholders. If BP was serious about a disciplined approach to capital expenditure, it would extend that discipline to its upstream business.

“Long-term investors want to see BP taking a genuinely disciplined approach to capital allocation to protect shareholder value through the energy transition.

“This research shows that growing upstream capex and expanding exploration is likely to be an irresponsible use of shareholder capital, the opposite of what is required from a 'fundamental reset'.

“BP’s pre-FID portfolio does not sit on the low end of the cost curve. The company’s high oil price assumptions, declining exploration success rates and rising discovery costs all increase the risk that sanctioning new projects could erode value.

“The rationale for continued exploration spending is increasingly unclear. BP’s exploration efforts have grown more expensive and less successful over time, raising serious questions about the value this can deliver for shareholders.”

Cllr Doug McMurdo, Chair of the Local Authority Pension Fund Forum (LAPFF) said:

“As long-term investors in BP, we want to see the company taking a genuinely disciplined approach to capital allocation to protect shareholder value through the energy transition. As part of the company’s ‘fundamental reset’, we expect bp to be able to explain how growing upstream capex and expanding exploration can truly be viewed through the lens of capital discipline.”

Harry Ashman, Senior Engagement Specialist, Robeco said:

“Investors are increasingly scrutinising the resilience of ongoing upstream and exploration spending as the energy transition marches on, and this report supports calls for further capital discipline in the oil and gas sector. It highlights an alternative path that could improve companies’ resilience, increase shareholder returns and reduce emissions. At Robeco, we remain committed to the net-zero transition to benefit our clients and create long-term value while balancing risk, return and sustainability; research like this demonstrates how these aims can be mutually reinforcing.”

]]>BHP can't ignore the writing on the wall for Saraji East, regardless of government go-ahead 2025-11-26T00:00:00Zhttps://www.accr.org.au/news/bhp-cant-ignore-the-writing-on-the-wall-for-saraji-east-regardless-of-government-go-ahead/ACCR is commenting on the Queensland Government’s recommendation that the BHP Mitsubishi Alliance’s (BMA) Saraji East Mining Lease Project is suitable to proceed.

Located in the Bowen Basin, Saraji East is a metallurgical coal mine awaiting Final Investment Decision from the BMA joint venture. The proposed mine is adjacent to BMA’s existing Saraji site and is expected to operate for around two decades and produce 110 million tonnes of coal.

The Queensland Government’s Environmental Impact Statement (EIS) indicates that the mine will generate around 18 million tonnes of direct emissions. The report estimates that 451 MtCO2e of scope 3 emissions[1] will be generated from the project, primarily from use of the mine’s coal in steelmaking.

The recommendation is not final and the proposal for Saraji East will now go to the desk of Federal Environment Minister, Murray Watt, for further consideration.

Commenting on the announcement, ACCR Head of Engagement and Sector Strategy, Naomi Hogan said:

“Despite a state-level recommendation, there is no indication BHP will advance Saraji East toward development. Rising labour and energy costs, alongside the return of metallurgical coal prices to long-run averages, have squeezed BMA’s margins in Queensland. It is difficult to make the case that Saraji East would stack up financially.

“The recent decision to mothball Saraji South, among other mines, shows that Queensland coal operators are already facing significant economic challenges. Investors will rightly ask about Saraji East’s viability when nearby projects are being sunk by rising costs, tight margins and mounting transition risk.

“In a world where steelmakers are increasingly planning for low-carbon and coal-free technologies, greater scrutiny of any new potential coal investments is a must. BHP should clarify for investors how Saraji East aligns with its ambition to support lower-emissions steelmaking and reduce scope 3 emissions.

“Communities and workers in the region will require assurances from BHP that any future investment supports long-term economic resilience. Transition impacts are increasingly central to how investors assess project risk.”

Background

Earlier this year, BMA placed Saraji South into care-and-maintenance, due to economic challenges, raising further questions about long-term project economics in coal.

]]>Leadership update at ACCR2025-11-13T00:00:00Zhttps://www.accr.org.au/news/leadership-update-at-accr/From January 2026, ACCR will adopt a co-leadership model, with Brynn O’Brien and Nick Kelly serving as co-CEOs. This deliberate and strategic evolution strengthens ACCR’s capacity to drive impact across our global footprint.

The world stands at a critical juncture. Current trajectories of global greenhouse gas emissions put us on a path toward temperatures that pose systemic risks. As an organisation dedicated to mitigating those risks - for investors, planetary systems, and people - our best work is collaborative, multi-jurisdictional, and focused on systems-level impact. A co-leadership model will enable us to achieve this more effectively.

Nick joined ACCR in July this year, leading ACCR’s multidisciplinary analytical and communications work. He brings experience at the intersection of climate, philanthropy, and legal strategy, with a background in legal practice, including as a barrister, in complex inquiries, public and environmental law, and public law teaching.

Howard Pender, Chair of ACCR, said:

“This change reflects ACCR’s commitment to strong, collaborative leadership as the organisation matures and tackles increasingly complex challenges. Brynn and Nick bring complementary skills and shared vision, and the board is confident this approach will position ACCR for even greater impact.”

Brynn O’Brien, Executive Director ACCR, said:

“I’m really excited about this next chapter of leadership with Nick. Co-leadership gives us the bandwidth and flexibility to take on more, stay connected across our work, and drive meaningful change in this crucial moment.”

Nick Kelly, incoming Co-CEO ACCR, said:

“I’ve been a huge fan of Brynn’s and ACCR’s work for years now. That view has been turbocharged since coming into the organisation earlier this year, so I couldn’t be more thrilled and humbled by the opportunity to work alongside Brynn to help ACCR have the impact the world needs in the second half of this critical decade.”

]]>BHP backflips on Mt Arthur coal wind down for 2030 – sells off land to coal miner instead 2025-11-03T00:00:00Zhttps://www.accr.org.au/news/bhp-backflips-on-mt-arthur-coal-wind-down-for-2030-–-sells-off-land-to-coal-miner-instead/The Australasian Centre for Corporate Responsibility (ACCR) is commenting on the announcement by BHP today outlining is has transferred just over half (3700 ha.) of the land and tenements associated with the Mt Arthur coal mine site to Malabar Resources, a neighbouring coal miner.

Commenting on the transfer, Naomi Hogan, Head of Engagement and Sector Strategy at the Australasian Centre for Corporate Responsibility (ACCR) said:

“BHP’s decision to sell land at Mt Arthur, and enable ongoing coal mining and burning post-2030, is a concerning backflip that will have impacts on investors, workers and the environment.

“We are concerned that investors have not received a proper level of transparency here, with BHP saying very little about the likely and significant additional emissions that will be created due to this transfer.

“The fanfare BHP brought to its 2022 announcement of a 2030 Mt Arthur closure – which demonstrated a balance between sound economic management, emissions reductions and fair workforce planning – now appears to have been hollow signalling.

“BHP gave the market the impression it had abandoned plans for coal divestment at the Mt Arthur site, but it is now revealed that the company has not given up on the proceeds from the remaining coal resources sitting underneath.

“Investors have long taken an interest in the site closure and emissions reductions at Mt Arthur, using it an important case study in just transition principles for workers, but today’s decision will test confidence in BHP’s strategy.

]]>New research: Shell’s LNG lobbying clouds its Paris commitments2025-10-30T00:00:00Zhttps://www.accr.org.au/news/new-research-shell’s-lng-lobbying-clouds-its-paris-commitments/Shell’s investors still lack clear visibility over the company’s lobbying activities - including whether they are Paris-aligned and how they support Shell’s LNG growth strategy - new ACCR research finds.

Commitment Issues: Shell's LNG lobbying risks undermining its Paris pledge identifies numerous instances of Shell lobbying in key emerging markets for higher, long-term gas and liquefied natural gas (LNG) use – activities that do not appear aligned with Paris pathways or the company’s commitment to lobby in support of the Paris goals.

While investor pressure led to Shell incrementally improving its lobbying disclosures over the past year, the research shows this has not delivered investors with adequate insight into the extent and impact of the company’s lobbying. Its disclosures do not address the tension between Shell’s ambitious LNG growth strategy, which does not appear Paris-aligned, and the company’s commitment to lobbying in line with the Paris Agreement.

Key findings:

Investor pressure has seen Shell incrementally improve its disclosures and acknowledge its lobbying engagement in emerging markets. However, investors still do not have adequate insight into the impact or Paris alignment of Shell’s lobbying, or the extent to which its lobbying supports and shapes strategy.

The report analyses Shell’s long-standing lobbying in four emerging markets which are material for Shell’s gas and LNG business, and where Shell has recently added climate-related lobbying disclosures:

China: Shell used its scenario modelling to promote Paris-misaligned gas use to policymakers for more than a decade. Its scenario modelling likely influenced China to pursue a more expansionary gas policy during its 13th Five Year Plan (2016-2020). Shell continues to advocate for elevated Chinese gas use in its scenarios, but it is unlikely to maintain its influence given policy and technology headwinds.

India: Shell used its scenario modelling to increase its access to policymakers and funded a study which appears to have influenced policy for developing a domestic LNG trucking market. This is despite LNG trucking not having clear greenhouse gas emissions benefits in India.

Malaysia: Shell lobbied for long-term gas use directly and via the Malaysian Gas Association (MGA), where it is a key member. The MGA helped shape Malaysia’s National Energy Transition Roadmap and endorses its plan to significantly increase gas use while targeting net zero by 2050. This contradicts Shell’s modelling of Malaysian decarbonisation, developed with a government climate agency, which contains much less gas and more renewables.

Nigeria: Shell is extensively involved in shaping the government’s Decade of Gas policy initiative, which aims to make Nigeria “gas-powered” by 2030. By targeting large increases in gas production and consumption, it risks pushing Nigeria’s rapidly growing economy onto a heavy-emitting development pathway.

Commenting on the research, Nick Mazan, ACCR Oil and Gas Strategy Lead, said:

“While strong investor pressure has driven some improvement in Shell’s lobbying disclosures, it seems that investors are still unable to properly assess the Paris alignment of the company’s lobbying and its relationship to Shell’s strategy.

“Shell’s improvements to its disclosures have not adequately addressed the friction between its advocacy for gas and LNG growth, and its pledge to lobby in line with Paris.

“Shell’s LNG growth strategy is a gamble on LNG playing a major role in the energy mix of emerging markets. As such, the company may have an incentive to lobby for increased gas and LNG use at the expense of its commitment to Paris-aligned lobbying.

“It may well be the case that Shell will not materially change its Paris-misaligned lobbying while its corporate strategy remains Paris-misaligned. Tackling the source of the inconsistency via ongoing scrutiny of Shell’s LNG growth strategy remains an important pathway for investors.”

Background

Over the last two years, ACCR has published extensive research and analysis that addresses Shell’s lobbying:

]]>New research: Grid-scale batteries untapped opportunity for Japan’s major electric utilities2025-10-23T00:00:00Zhttps://www.accr.org.au/news/new-research-grid-scale-batteries-untapped-opportunity-for-japan’s-major-electric-utilities/New ACCR research finds there is commercial benefit for Japan’s major electric utilities to increase investment in grid-scale battery storage.

Japan’s regional electric power companies (EPCOs) and largest wholesale generator (J-POWER) appear increasingly misaligned with the country’s recent efforts to decarbonise its energy system. The utilities’ business models are built around centralised baseload demand, whereas renewables and decentralised supply have become progressively important to the grid.

With rising rates of curtailment – wasted renewable energy – in Japan, grid-scale batteries can provide more energy storage capacity and the flexibility to deploy it when needed.

The utilities covered in the research have a competitive advantage in the battery market, as they own most generation assets and grid infrastructure while having regional operational expertise. However, they need to act now to secure first-mover advantage.

Key findings

Batteries are already capable of commercial viability in Japan – There are opportunities to earn above a 10% internal rate of return (IRR) via multiple revenue streams – capacity payments, energy arbitrage and ancillary services payments – supported by government subsidies.

Battery costs are plummeting – The global levelised cost of electricity (LCOE) for battery storage dropped from US$300/MWh in 2018 to US$104/MWh in 2024. BloombergNEF (BNEF) analysis expects this to halve again by 2035. The cost of building and operating new batteries will soon be cheaper than the cost of running existing LNG plants in Japan.

Deploying batteries will help Japan make the most of its growing wind and solar energy – Existing storage capacity, primarily provided by pumped hydro, is no longer sufficient as renewable generation grows. Market forecasts suggest a significant scale up of batteries, with BNEF estimating a tenfold increase in storage volume from 2023.

Commenting on the report, Martin Norman, Investor Engagement Lead, ACCR, said:

“Our report shows that an important window is now open for Japanese utilities on battery investment. The conditions for battery investment are favourable and with such a strong business case it is only a matter of time before there is broader commercial uptake.

“However, time is of the essence, making it crucial that investors engage with Japan’s electric utilities to ensure they are acting to guarantee a first-mover advantage.

“Electric utility companies in Japan, many of which are highly leveraged, remain focused on centralised baseload despite operating in a grid increasingly reliant on renewable energy supply. Investors are eager for more prudent capital allocation. The low cost of batteries, and their ability to contribute to Japan’s energy transition, offers big wins – if companies move now.

“Japan’s electricity utility companies must be considering grid-scale batteries in their decarbonisation and capital allocation decisions. If they aren’t, the question is, why not?”

]]>NBIM’s Climate Plan falls short of its own warnings on risk; but focus on corporate lobbying and board scrutiny welcome2025-10-22T00:00:00Zhttps://www.accr.org.au/news/nbim’s-climate-plan-falls-short-of-its-own-warnings-on-risk-but-focus-on-corporate-lobbying-and-board-scrutiny-welcome/The Australasian Centre for Corporate Responsibility (ACCR) is commenting on Norges Bank Investment Management’s (NBIM’s) 2030 Climate Action Plan, released today.

Brynn O’Brien, ACCR’s Executive Director, said:

“NBIM is a clear leader in understanding and communicating the scale of climate-related risk. But there remains a widening gap between the systemic risk the fund itself describes and the scale of action it proposes in response.

“Much of the plan focuses on refining analytics, disclosure and engagement — all important tools. What’s missing is a shift from describing the risk to actively helping to reduce it. Managing exposure to risk is not enough when the risk itself threatens the long-term stability of markets.

“For a universal owner with a mandate to safeguard value for future generations, the fiduciary duty to manage climate related risk is inseparable from mitigation -- taking action to reduce the likelihood and severity of systemic climate risks. Fulfilling that duty means using influence to drive mitigation, not just monitor consequences.

“The fund’s commitment to increased scrutiny of corporate policy advocacy as it relates to climate change is new and very welcome, as is the explicit acknowledgement of voting against boards as an escalation tool. However, we continue to see critical gaps: the need for stronger and more transparent company stewardship, clearer thresholds for escalation where engagement fails, and a commitment to not finance new fossil fuel infrastructure. Leadership in this decade means using every available lever to help prevent the worst outcomes.”

]]>AGL shareholders keep foot on the transition accelerator2025-10-03T00:00:00Zhttps://www.accr.org.au/news/agl-shareholders-keep-foot-on-the-transition-accelerator/The Australasian Centre for Corporate Responsibility (ACCR) is responding to the shareholder vote on AGL’s Climate Transition Action Plan (CTAP), which received a nearly 31% vote AGAINST at the company’s Annual General Meeting, held today.

Commenting on the vote, Brynn O’Brien, Executive Director at ACCR, said:

“A sizeable chunk of AGL’s shareholders have used their votes to keep the pressure on Australia’s largest corporate emitter over its climate strategy. Nearly 31% of shareholders voted against AGL’s Climate Transition Action Plan today, matching the vote against the plan the company presented in 2022.

“This sends an unambiguous signal to AGL’s board and executives that the company needs to do more to drive the energy transition. AGL must move quickly to deliver real emissions cuts and a more compelling strategy that seizes the opportunities of the energy transition.

“AGL is still not Paris-aligned and its slow pace risks holding back the entire country’s transition. The new CTAP leaves the company out of step with Australia’s newly announced 2035 emissions target.

“AGL’s plan, which proposes no further reductions in gas emissions for the next decade, gives little confidence that company leadership is up for making the hard choices surrounding gas and its increasingly unreliable coal assets.

“To benefit from the transition, AGL needs to make big structural changes to its business, but its plan has major gaps: it fails to accelerate renewable buildout, ignores emissions from gas supply, and the electrification strategy lacks credibility, while coal closure dates remain too late.

“Shareholders have sent a clear signal: AGL must stop hedging and start leading by delivering a timely decarbonisation strategy.”

Background

ACCR’s analysis of AGL’s 2025 Climate Transition Action Plan can be found here.

AGL’s previous CTAP received a 30.69% vote AGAINST – making it the third worst ‘Say on Climate’ vote on record at the time.

]]>“Ignoring these confronting warnings will simply be negligent”: Australia’s National Climate Risk Assessment sounds the alarm for investors2025-09-15T00:00:00Zhttps://www.accr.org.au/news/“ignoring-these-confronting-warnings-will-simply-be-negligent”-australia’s-national-climate-risk-assessment-sounds-the-alarm-for-investors/The Australasian Centre for Corporate Responsibility (ACCR) is commenting on the release today of Australia’s first National Climate Risk Assessment.

While risks to the economy are classed as "moderate" today, they escalate substantially to become "very high" by 2050.

Current impacts include:

Insured losses from declared insurance catastrophes have grown from 0.2% of GDP (or $AUD2.1 billion) in 1995–2000 to 0.7% of GDP (or $AUD4.5 billion) in 2020–2024.

In 2024, 15% of household insurance premiums could be priced at more than 4 weeks of gross household income, a 25% increase from 2023.

By 2050, the climate risk evaluation from the Australian government rises to “very high”, with:

Losses in Australian property values are estimated to increase to $AUD611.0 billion by 2050 and could increase to $AUD770.0 billion by 2090

Between 700,000 (+3.0°C) and 2.7 million (>+3.0°C) additional days of work are projected to be lost every year by 2061 due to the higher frequency and intensity of heatwaves, particularly affecting agriculture, construction, manufacturing and mining.

It is estimated that labour productivity could decrease by 0.2% to 0.8% by 2063, which would reduce economic output by between $AUD135 billion and $AUD423 billion.

Climate-driven events could result in cascading shocks to the financial system. Financial system shocks or volatility can be triggered by asset write-downs or loan defaults across a region, with potential ripple effects for households and businesses by reducing access to finance, the value of investments or superannuation.

Brynn O’Brien, ACCR’s Executive Director, said:

“The National Climate Risk Assessment lays bare a confronting and terrifying reality -- climate risk is here, now, and escalating across every part of our economy and society. It’s clear why the government delayed releasing this report. But delay doesn’t make the risks go away. It only makes them harder and more costly to manage.

“We expect long-term investors – especially investors who have to look out for the interests of their beneficiaries retiring in 30 or 40 years - to be deeply worried. Climate change will erode returns across sectors and geographies. Diversification won’t protect portfolios.